Michael Saylor, chairman of MicroStrategy is a well-known promoter of bitcoin. What is not so widely appreciated is that MicroStrategy is aggressively issuing convertible debt denominated in fiat to buy yet more bitcoin — it is leveraging its balance sheet to do so. According to a Financial Times Alphaville column, MicroStrategy has issued its fifth convertible this year:

“…a $3bn, five year note with zero per cent coupon and a 55% conversion premium to a share price that was already trading at nearly three times the net asset value of its bitcoin holdings — all to fund its relentless quest for more bitcoin.”

The implication is clear: this is a price ramp in a strictly limited market. Coupled with bullish promotion, it is done in a way bound to discourage sellers and to make Saylor and his company extremely rich — in Federal dollars of course.

Nearly every owner of bitcoin has bought them anticipating speculative, even spectacular profits measured in their national currency. And even the evangelists delude themselves when they espouse higher monetary ideals.

I have little doubt that MicroStrategy’s scheme of puffing up the price of bitcoin could push it even higher in the short-term. And there are and will be imitators: the FT article cites bitcoin miner Mara with $850m in convertibles, refinancing debt and buying more bitcoin. But bitcoin is inherently unstable, with all the characteristics of a spectacular bubble.

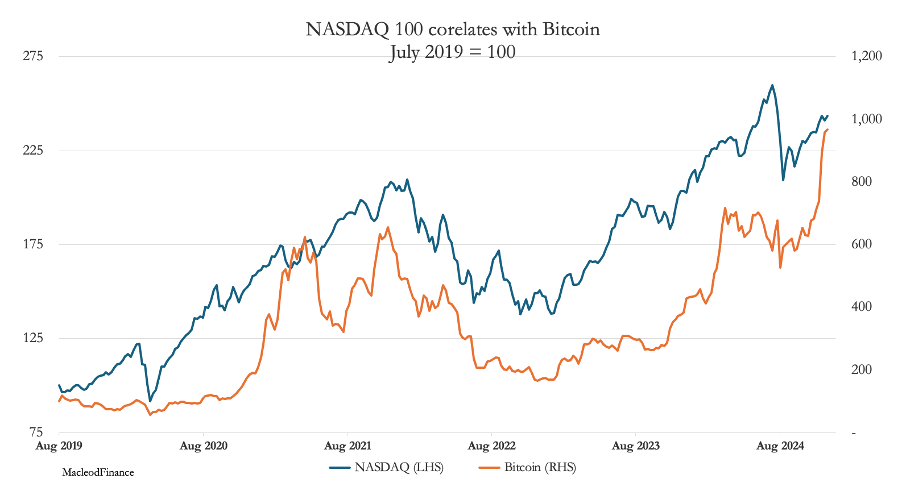

Bitcoin’s crowd is the same cohort fuelling the tech bubble, as the correlation with the NASDAQ index clearly demonstrates:

Both tech stocks and bitcoin are driven by momentum buyers: buyers who buy because they are rising and not on value considerations which they ignore. And equally, when values decline, they sell — again, this is momentum potentially becoming a panic, never based on value considerations. The dangers of markets driven purely by momentum were illustrated in the tech bubble of 2000. Make no mistake, bitcoin is not money and bubble conditions have returned.

This begs the question, as to why Saylor is pushing the US Government to adopt bitcoin as a replacement for gold. This hope is traduced by reality on all levels. But most importantly, if the US government does as Saylor says, it would become his exit from bitcoin having pocketed billions in old-fashioned fiat dollars.

However, the US Treasury is unlikely to follow Saylor’s advice. For one thing, it would add legitimacy to hundreds of billions’ worth of criminal transactions including the proceeds of crime and money laundering. And far from being a slam-dunk escape from statist currencies, the future of bitcoin depends entirely upon the tolerance of governments whose currencies stand to be undermined by it. This should not be dismissed lightly.

Bitcoin’s status in common law is not as money, while that of gold (and silver for that matter) is money. But in a modern economy, money is hardly ever used in transactions, but it is credit which circulates. And if you want to stabilise the value of credit, you must tie it to gold whose value has proved to be stable over long periods of time — not bitcoin which is inherently unstable. Promoters of bitcoin as the future money are clearly ignorant of these facts, as are, sadly, those in the media who question them.

There is also legal uncertainty over bitcoin’s status as property. Fungible goods, such as money and credit, are irrecoverable if stolen and passed on to other parties. Thus, if someone steals your cash and spends it in a shop, even if you marked the notes or made a note of the serial numbers you have no redress in law against the shopkeeper, unless it can be proved that he was in league with the thief. This differs from non-fungible property, such as household goods, which are recoverable by the original owner without compensation, even if they enter into the possession of an innocent party.

This is where the blockchain complicates things for bitcoin. It gives an identity to each bitcoin and Satoshi in possession, which if they were deemed to have been previously acquired through the proceeds of crime or money laundering could jeopardise subsequent possession. Doubtless, different jurisdictions will interpret the laws of possession in their own way with reference to common law. But bitcoin hodlers are generally unaware that they do not have clear title to bitcoin in their possession, even though the blockchain suggests they that they do.

With these uncertainties, bitcoin has all the attributes of an ephemeral financial bubble, a scam perpetrated on an avaricious public. In a recent Fox Business interview, Saylor continued to fuel this speculation, projecting its value to $13 million per coin by 2045. If there’s a motive in his statement it is to push the price higher. Whether it is motive or ignorance of monetary facts, there appears to be little difference in principle between this promotion and that of John Law and his Mississippi venture in 1718—1720 France.

A risk bitcoin speculators now face is governments acting to preserve the credibility of their fiat currencies. If bitcoin is seen as a threat to the stability of a major currency, governments will act to kill it. And given the correlation with NASDAQ, it will also be unlikely to survive that bubble being popped.

Just add it to the catalogue of extraordinary popular delusions and the madness of crowds.