This article points out the dangers to the value of credit from a rickety global banking system. This will almost certainly become the primary driver in the gold to credit relationship, replacing the so far relatively benign downwards long-term drift in currency purchasing powers. In other words, it is increasing awareness of systemic risk and debt traps that will drive the relationship, not false theories about interest rate differentials.

The entire western banking system is close to collapse

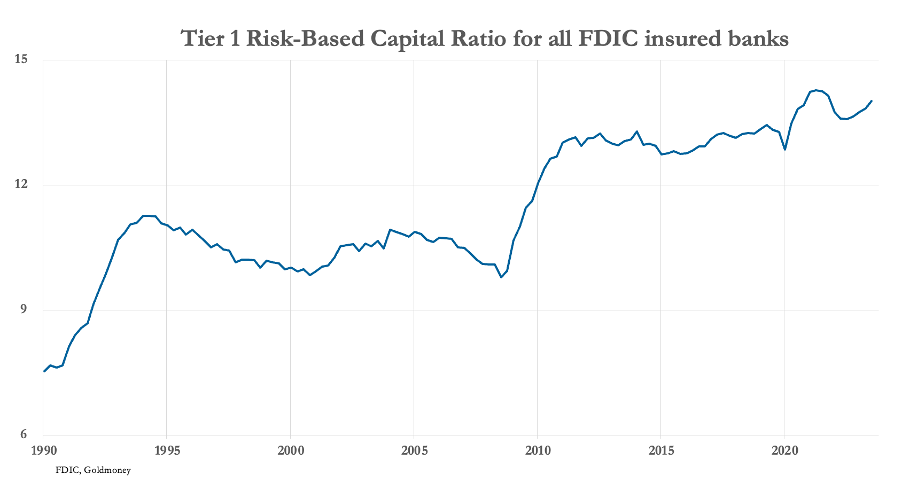

Because there is an apparent lull in the banking crisis, it has disappeared from the headlines. But that doesn’t mean it has gone away. A further deterioration in bank balance sheets will undoubtedly call into question the values of individual bank counterparty credit, entire banking systems, central banks, and currencies themselves. Let us remind ourselves of where we are in the bank lending cycle by looking at the relationship between bank equity capital and their balance sheets. The chart below shows the aggregate position for the entire US banking system.

It is as plain as a pikestaff that this ratio has been rising for as long as the Federal Deposit Insurance Corporation has been collecting these statistics — 34 years. The point about high balance sheet leverage is that it doesn’t take much in the way of loan losses to bankrupt a bank.

The chart tells us that the banks have responded to the trend for ever lower interest rates by increasing their balance sheet leverage to grow their profits at a time when credit margins became increasingly compressed. To describe the condition as a lending bubble is not an exaggeration, and we know that all bubbles burst eventually. Unfortunately, the US banking system is the best of a bad bunch. The balance sheet leverage in the large international banks in the Eurozone and Japan is considerably higher, close to twenty times. Undoubtedly these excesses can be linked to the negative interest rate regimes imposed formerly by the ECB’s euro system and still by the Bank of Japan.

Some vitally important questions arise: what will pop these lending bubbles, how will they be dealt with, and what are the consequences for the value of credit expressed in the gold to credit price relationship?

The consequences for interest rates

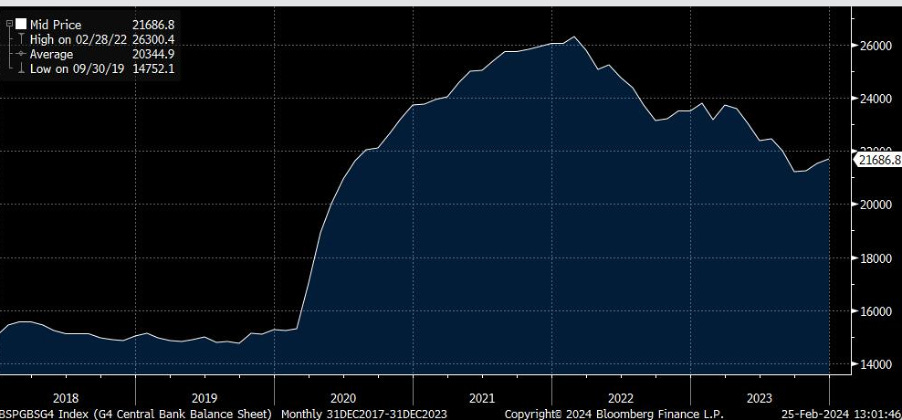

The undoubted threat to the entire credit system arises from the inflationary consequences of covid in particular and how the massive expansion of central bank balance sheets from the first covid lockdowns fed into consumer price inflation. Exacerbated by sanctions against Russia, this inflation shock led to a sharp rise in dollar interest rates, catching some regional US banks unawares. While few in official circles will openly admit it, the subsequent reduction in central bank base money through quantitative tightening was more responsible than anything else for reducing headline inflation. The chart below shows how the combined balance sheets of the Fed, ECB, Bank of Japan, and Bank of England have contracted since Q1 in 2022.

It is wasteful expansion of central bank credit which has most impact on a currency’s purchasing power. But quantitative tightening from early 2022 is now over, and we can expect QE to return to ease national debt traps. Debt management must be prioritised over inflation.

Even with a return to QE, the funding of government debt, particularly that of the US, can only be achieved at higher rates of interest. Other than perhaps a token dip in the Fed Funds Rate, it simply cannot fall to the extent discounted in financial markets. It is only a matter of not much time before this reality informs investors’ expectations.

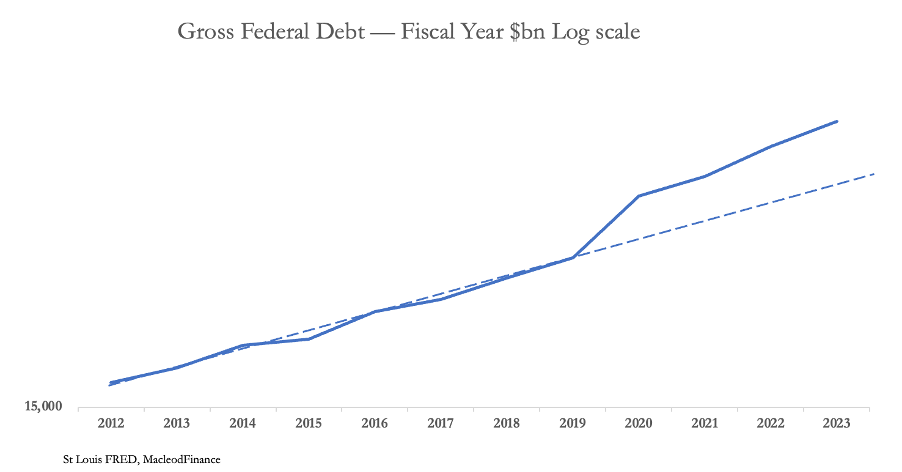

That the US faces a debt trap crisis is best shown by the chart below.

The pecked line shows that in real terms (adjusted logarithmically) the growth of gross Federal debt was steady until fiscal 2019, since when it has accelerated. When the economy was effectively shut down during the covid crisis, the jump above this trend came as no surprise. But what is not generally appreciated is that the gap between debt growth and the pre-covid trend is still widening. Furthermore, the chart does not include post-2023 September debt, which has increased by $1.3 trillion representing a further acceleration of trend to a $3+ trillion budget deficit for the current fiscal year.

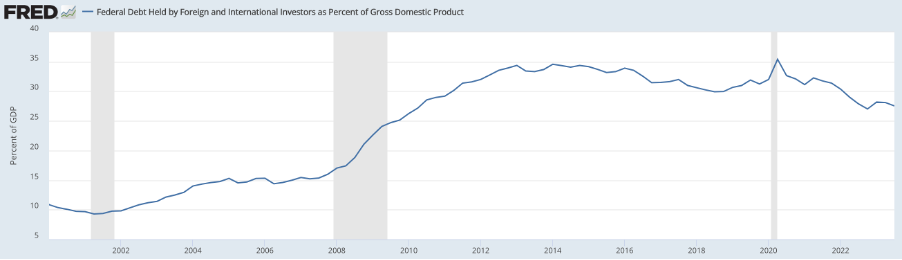

Funding this accelerating debt includes rolling in a compounding interest element because the US Treasury doesn’t pay for the interest: it is simply rolled into tomorrow’s debt. The rising cost of funding being rolled into future debt is a classic feature of a debt trap as anyone who accumulates credit card debt will attest. The position is made worse by declining involvement of foreign investors, illustrated next.

In less than four years, foreign owned Federal Government debt has declined from 35% to 27.5% of GDP. And with China and Japan, the two largest holders actively reducing their exposure the ratio will continue to fall. The point is that at the margin it is foreign demand which will play an important role in determining the financing cost of the nearly $11 trillion of new and to be refinanced Treasury debt this year.

The evidence is clear, that with the US Government’s finances caught in an intractable debt trap and foreign buyers not adding to their positions US bond yields will continue to rise. The basic implications are as follows:

· Interest rates must continue rising in order to fund the Federal debt.

· Private sector debt will be destabilised, with malinvestments meeting their inevitable fate. Even formally profitable enterprises will be made insolvent by rising interest rates and their consequences for the financial and economic outlook.

· Accordingly, the economic slump has only started. It is set to become considerably deeper as interest rates continue to rise.

· Financial and property asset values will collapse along with rising bond yields.

· Financial asset values act as collateral for the entire system of over the counter and regulated derivative markets, which will require additional support. Will your stocks be mobilised for this purpose without your knowledge and consent? Legally, it is possible.

· A systemic banking crisis is bound to ensue, potentially far greater than the so-called Great Financial Crisis, which by comparison will be like a distant pimple on an expansive landscape.

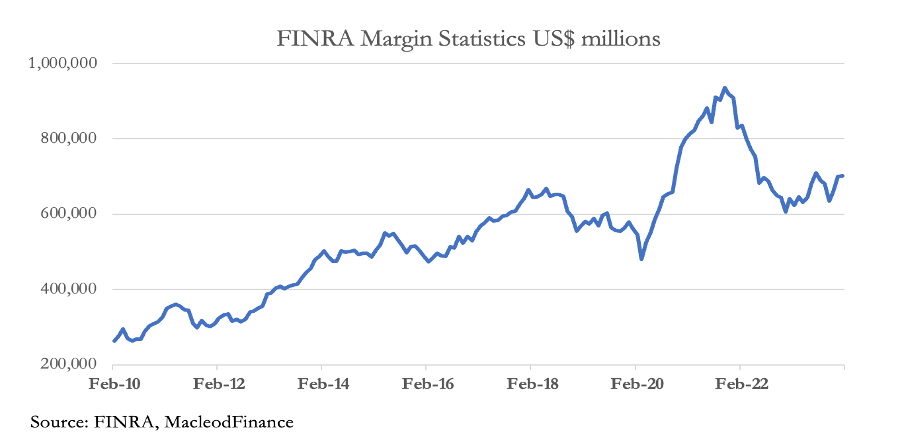

As these problems unfold, in order to survive commercial banks will call in loans where they can, panicked by the high degree of leverage on their balance sheets. Part of the loan liquidation, currently totalling nearly $702 billion according to FINRA will be from declining equity markets. The current loan position overhanging US equities is our next chart.

Having declined from all-time highs of $936bn, these loans are on a rising trend again, doubtless driving the tech bubble on Wall Street. We should not forget that it was collateral liquidation which fuelled the Wall Street Crash of 1929—1932, leading through a ripple effect to the collapse of an estimated 9,000 banks.

Given today’s high bank balance sheet leverage, it will take very little in the form of non-performing loans to collapse the entire commercial banking system. Of course, that cannot be allowed to happen and the burden of supporting all commercial banks will be the backstop responsibility of central banks and their controlling treasury ministries — just like when Lehman failed.

The backstop for a banking crisis is bust as well

A primary function of a central bank is to act as lender of last resort, a duty discharged by the Fed only last year under the Bank Term Funding Programme. But with government debt traps driving bond yields higher and collapsing collateral values, the entire burden of a massive systemic crisis in the commercial banking network from further increases in interest rates bankrupting their borrowers will have to be shared between the major central banks. But without massive capital injections, they themselves are technically bankrupt, concealing massive losses through their purchases of government bonds through QE. The only exception is the Bank of England which extracted a guarantee from the UK Treasury to take the losses.

In the case of the Bank of Japan, it has been doing QE for the last twenty-four years and its capital is wiped out thousands of times over. The entire euro system is riddled with balance sheet losses not only at the ECB but also among the national central banks.

Not only are their balance sheets in a mess, but their profit and loss accounts are taking a bad hit as well. All the major central banks doing QE ended up with bonds as assets sporting very low, or even negative yields. Now that interest rates have risen, the cost of financing these bonds is considerably greater than their coupon payments. In the euro system, the ECB recently unveiled losses of €1.3 billion, and the Bundesbank burned through provisions and reserves of over €20 billion last year — and there’s talk of a state bailout for the latter. Morgan Stanley estimates that the entire euro system faces P&L losses of €62 billion this year, after losing €56.6 billion last year. Note that these figures don’t include additional mark to market losses on bond holdings acquired through QE, which are being ignored.

One can understand why the Bank of Japan has refused to raise its deposit rate. With its massive holdings of bonds and even equity ETFs, the losses on its P&L account from higher interest rates would be simply horrendous, making a recapitalisation effort beyond the pale.

With all the west’s financial system backstopped by technically bankrupt central banks, a credibility crisis for the entire fiat currency system can be added into the mix. Investors will be staring down the barrel of not just the loss of value in their financial and other assets due to higher interest rates and bond yields, but the faith in the value of their fiat currencies, which are also credit, will be undermined as well.

Geopolitics and the consequences for investors

The threat from the dollar’s debt crisis to the entire global credit system has been long foreseen by both China and more recently Russia as well. In recent years, it is also seen as an increasing threat to their survival by Asian central banks and others in the Global South. This is why China, Russia, and their allies have been accumulating gold bullion, not just as declared by their central banks, but in sovereign wealth funds and other accounts to conceal the true scale of ownership. Furthermore, both these nations have invested in gold mine output and together now dominate global goldmine output.

At some stage, both Russia and China are bound to protect their currencies from a western credit crisis. They can only do this by establishing credible gold standards for the rouble and yuan. Indeed, for Russia it may even be in her strategic interests to do so deliberately to destabilise the dollar-based global credit system before it fails of its own accord. But she is currently restrained from doing so by China and India, evidenced by Russia’s proposal for a gold-backed trade settlement medium which failed to make the BRICS agenda last August.

American, British, European, and Japanese investors being almost entirely exposed to credit in the form of fiat currencies, bonds, and equities face the prospect of a total wipe-out. It is estimated that their exposure to gold and gold substitutes is less than one per cent of their financial assets.

While it is our own governments which have made this crisis, the entire Russia-China axis and their economic allies in the Shanghai Cooperation Organisation and BRICS+ form the silent majority of the world by both population and GDP. Therefore, while the impact of a western financial collapse will be extremely unpleasent, fortunately for us all there is a global majority capable of reintroducing gold standards to back their credit.

Meanwhile, the now inevitable collapse of the dollar, euro, pound, and yen will be reflected in far higher values for gold measured in these collapsing currencies. So far, it has not been gold rising, but these currencies declining. But at some stage there will be a currency to gold version of a crack-up boom, whereby desperate holders of fiat credit will dispose of it just to get their hands on bullion and gold coin irrespective of cost. It is now possible to discern this outcome, thanks to the final collapse of the rotten fiat currency system hoving into view.